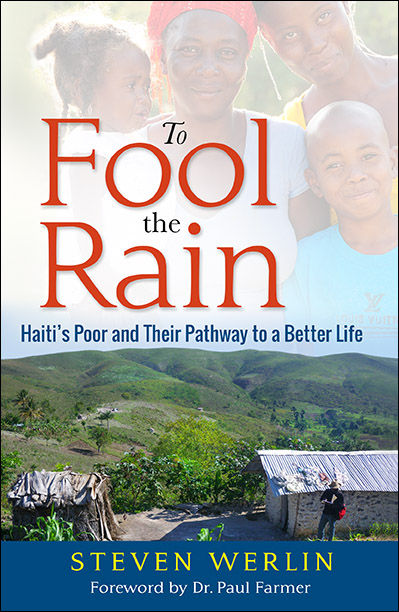

Review of “To Fool The Rain”

By the spring of 2011, I had become sufficiently invested in and intrigued by Fonkoze, a Haitian microfinance and social development institution, to publicly commit to writing a book about it. Several years before that, I had met Steve Werlin, one of the most unusual and wonderful men I have ever come across.

Think of him as a cross between the most thoughtful, soft-spoken graduate student you ever met and Buddha – a playful, intensely curious and humble man with no apparent concern for accumulating any material possessions beyond finding a strong cup of coffee to enjoy each morning and a place – anyplace, really – to get a few hours sleep every night.

A couple of years after I announced my intention to write a book about Fonkoze, Werlin quietly began talking about his desire to write one on Chemen Lavi Miyo (CLM), the organization’s signature program designed to uplift rural Haiti’s ultra-poor which I wrote about previously on this site here and here. While I continue to struggle to deliver on my commitment, Werlin has not only followed through but has written something truly unique and outstanding: To Fool the Rain: Haiti’s Poor and Their Pathway to a Better Life.

Over the course of 27 reader-friendly (meaning short) chapters, he introduces a handful of CLM clients and the staff, called case managers, who serve them. Through deft story-telling, we learn about an arduous 18-month process of building up clients’ income, assets, confidence, social standing, ability to plan, and, in the end, their humanity. He lets us see the violence, absurdities, superstitions, beauty, and mundane realities of rural Haiti along the way.

Some stories end in qualified triumph and a few in tragedy; others conclude ambiguously. While he does not make himself a central character in the book, he does not disappear either; in this and other ways, he achieves an effective balance that a less able writer would have failed at.

He has a way of stating profound truths starkly, informed by a keen eye for detail. To wit:

Regarding outsider’s roles in Haiti: “Americans and other foreigners have been coming to Haiti for years bearing all sorts of gifts and doing all sorts of harm.”

On not getting enough to eat in rural Haiti: “Adults may hide hunger. Children generally don’t.”

About CLM client named Manie: “Her high, soft voice is clear, but always sounds a little weary. She doesn’t speak. She sighs.”

Steve Werlin with a Fonkoze Family in Ench

Or this about a case manager named Martiniere as he talks with a woman who was about to give up on the program after a demoralizing setback: “As she spoke, his every gesture – the way he nodded now and then, his smiles, his scowls, the way he shook his head – let her know that he understood.”

For me, the highlight of the book was the conclusion of a story about a woman named Josamene Loréliant. She was so downtrodden that virtually everyone she knew called her a nickname, Ti Rizab, which basically signified that she was not a human being, but rather a bad joke. She accepted that appellation for her entire life until she accumulated assets, a tiny but sturdy home that most Americans would consider a small shed, and some measure of confidence. By the time she graduated from CLM, Werlin tells us, she insisted that people call her by her proper name.

Some years ago, Werlin wrote a teaching tool for Fonkoze microfinance clients based on stories of rural Haitian women going through their daily lives. A senior Haitian employee of Fonkoze who is both a feminist and nationalist told me that she was at first incredulous, and later simply astonished, that an American man – yes, Steve Werlin – had written so effectively from the point of view of a Haitian woman.

I had always hoped that Werlin’s improbable gift for seeing the world through their eyes, and his unique experience of being part of a team that painstakingly helps to transform their lives, would come together in a book that could help foreigners like me who have a desire to understand and help Haiti. Well, he has done just that.

The Author of To Fool The Rain

Werlin waits until the final few paragraphs of this slim volume to tell the reader that CLM has achieved and maintained a 95% success rate. Unlike so much philanthropic writing these days, he does not lead with data, abstractions or buzzwords. Human stories gleaned from endless trips to talk to people in their native language, meeting them where they are (literally and figuratively) in order to nudge them forward on a pathway to a better life, are at the core of To Fool The Rain. The fact that this program has been proven, through rigorous impact evaluation research, to work in multiple countries with populations that most development specialists had effectively written off is, oddly and wonderfully, a secondary point in Werlin’s captivating story.

At the very end of the book, this skinny, self-effacing man mounts a small soapbox and writes with great moral clarity: “Extreme poverty exists because we chose not to eliminate it.” Very few people have earned the right to credibly pen such unambiguous words. Steve Werlin, at the conclusion of To Fool the Rain, is one of them.

A Tribute To Matt Balitsaris

On a recent night in Boston I joined a dinner honoring Matt Balitsaris, a philanthropist who has worked in solidarity with the Haitian people for a long time, and who succeeded me as Chairman of Fonkoze USA. Towards the end of the evening, I gave him a toast, and others did as well. A reconstruction of my toast appears below.

A wise man, who happened to be my father, said to me once that when you properly say farewell to a departing employee or volunteer, you are doing it as much for the people who staying as you are for the person who is leaving. By that I took it to mean that the organization is signaling that it values good work done the right way, which applies to everyone. So Matt, I know you may find this ceremony tonight a little embarrassing, as you are a truly humble man, but perhaps you can recall that by honoring you we are honoring all those who serve Fonkoze and Haiti.

I served as Vice-Chair before I was elected Chair of Fonkoze USA in November 2009. Mary Becker was the Chair at that time, and she involved me in many important ways. Mary and her husband Gary were two of the true giants of this organization’s history. But when I was elected Chair, I imagined a more robust role for the Vice-Chair. In part this was because my ambitions for Fonkoze during my time as Chair far outstripped the amount of time I could give, and also, frankly, my capabilities.

I served as Vice-Chair before I was elected Chair of Fonkoze USA in November 2009. Mary Becker was the Chair at that time, and she involved me in many important ways. Mary and her husband Gary were two of the true giants of this organization’s history. But when I was elected Chair, I imagined a more robust role for the Vice-Chair. In part this was because my ambitions for Fonkoze during my time as Chair far outstripped the amount of time I could give, and also, frankly, my capabilities.

I did not know Matt that well, but we quickly began working together very effectively. He gladly took on the wider mandate for Vice-Chair – which effectively amounted to him being a Co-Chair. (In this sense, he served as Chairman for six years, rather than just three.) This arrangement turned out to be essential, since it was about ten weeks after I was elected Chairman that the earthquake struck in January 2010. There was more than enough work for both of us to do.

In fact, you could say that this enhanced role was akin to George W. Bush elevating the role of Vice-President for Dick Cheney. Well, maybe that’s not the best example actually.

Matt has a certain style. Do some of you recall the TV show and character Columbo, and how Peter Falk played him? You had this rumpled detective who led everyone to believe he was dim-witted, which caused the villain each week to under-estimate him. But when it mattered, Columbo would show his keen intellect and how effectively he could get things done.

Matt operates in much the same way. He is typically underestimated, and I believe that also helps him get things done. People often don’t notice how smart he is, even after he has gotten something done – usually while leaving few if any fingerprints!

Yet, like Julian Schroeder – another Fonkoze hero – when needed he can shed his laid back persona and bring forth strong views, strong leadership, and even strong language. And when that moment, usually some kind of crisis, passes, he slouches back into his normal manner and quietly goes back to getting things done behind the scenes and through others.

Matt is someone who has deep knowledge of and commitment to Haiti over many years, and terrific contacts there. Unlike people like me, who had never gone to Haiti before I got involved in Fonkoze and may never return now that my term is complete, Matt had been going there for years before he was elected to the Board, learning and contributing at each step. I am sure he will continue far into the future.

One of the many things I appreciate about Matt is that when he learns something that contradicts his point of view on an issue, he is willing to change his point of view and also let people know, even those who had had argued with previously on the issue. At the risk of reinforcing a gender stereotype, I find that men are particularly averse to changing their mind and even more to letting others know they have done so. This is true even when sharing your change of heart would build rapport and trust. Matt is an exception to that rule, and his example has spurred others to change their minds, build trust, and create an environment where people are humble and curious.

Let me offer one final observation. Being that this is Fonkoze, we do certain things a lot. For example, we drink wine. We go to Haiti. We raise money. And we argue.

Matt has this ability to have everyone who is in an argument believe that he is on their side. Sometimes people achieve this by saying different things to different people. But that’s not Matt’s approach. He is consistent and tells the truth, the same truth, to all sides.

You see, it is clear to everyone that at the end of the day when people are feuding, Matt does not take one person’s side or the other. Rather, he takes the side of the women of Fonkoze, and the women of Haiti. His principled and values-led approach makes has earned the respect of everyone in Fonkoze, whether they agree with him or not on any particular issue. This way of operating has also created a standard that many of us aspire to, even though few of us attain it.

So, for the good of our mission, as we pass this milestone we should not only thank Matt, but also each of us would do well to get in touch with our inner Matt Balitsaris as we confront the opportunities and challenges ahead.

The Success of Graduation Programs for the Ultra Poor, Microcredit, and Fonkoze

Yesterday there was an important article in the New York Times by Nicholas Kristof about the graduation model, which is the generic term used to describe Fonkoze’s Chemen Lavi Miyò (CLM) program for the ultra-poor of Haiti. Kristof comments on the fact that early research has shown significant and sustained positive impacts on the clients of these programs in multiple countries. One of his themes is that reducing the stress the poor face and giving them hope-infused pep talks can actually help them a great deal – insights that are woven into CLM and similar programs, and also into behavioral economics based analyses of poverty which are becoming increasingly influential.

Unfortunately, Kristof comments negatively, in passing, about microcredit. This despite the fact that unlike graduation programs, microcredit is now being provided sustainably and on a massive scale globally by a network of microfinance institutions such as Sèvis Finansye Fonkoze (SFF), the financial services arm of Fonkoze. (The sustainable part has been a long time in coming for SFF, but based on recent performance, it has made substantial progress and making a profit this fiscal year is within reach.)

This tendency in the humanitarian sphere to pit innovations against each other in a kind of unhelpful “horse race” – rather than seeing how they can synergize and complement one another – is unfortunate as well. My view is that it is much less about graduation programs versus microcredit but rather, how these two social innovations can work together.

I wrote to Kristof and urged him to think in a more balanced way about microcredit, and directed him to my blog and this helpful article on microcredit research. He wrote me back and said he agreed with my blog on several key points. (The fact that he immediately read my long blog speaks well of his curiosity, which is a key character trait of great journalists.)

I think there is an important opportunity for SFF and the Fonkoze Foundation to show what they have learned and achieved in terms of actually graduating CLM clients to something that allows them to continue to make progress. This is important because even after achieving increased economic security, the formerly ultra poor “graduates” are still living precarious lives with minimal — albeit enhanced — assets and options.

SFF’s Ti Kredi and solidarity loan products and related services (some provided by the Fonkoze Foundation) have, in some cases, offered ways for CLM graduates to continue their forward progress and integrate into a heterogeneous and supportive social network (i.e., solidarity centers).

I have recently finished Walter Isaacson’s new book, The Innovators, about the people who brought us the information revolution – of which a surprising and unheralded number were women. As this blog has at times been used as a book review for titles that address or have implications for poverty alleviation efforts in Haiti and beyond, I will be posting some comments about it in the days ahead.

One of the themes that Isaacson cites again and again is the power of collaboration in spurring innovation – thereby bursting the bubble of the iconic images of Thomas Edison working alone in his lab or Steve Jobs in his garage, which purport to show that innovation often happens as part of a solitary pursuit. My own experience with Fonkoze and Grameen Foundation reinforces the power of well-constructed teams to drive waves of innovation that build on earlier discoveries and have the potential to reach scale sustainably.

Reflections on Haiti, Five Years After the Big Earthquake

When the ten-year anniversary of the Asian Tsunami was lurking a few weeks back, it prompted me to reflect on what I have learned about disaster response and recovery. In a blog published soon before the December 26 milestone, I emphasized the importance of leveraging, creating and enhancing local institutional capacity in order to make rebuilding sustainable – a way to give real meaning to the post-disaster cliché “build back better.” This theme was picked up in an AFP wire story that quoted me. Now the international community must confront the five year anniversary of the Haitian earthquake this month. Hopefully there will be more than just hand-wringing punctuated by the odd story on some well-intended church group or celebrity donor, and instead include some accountability for what has been (and has not been) accomplished and learned (see this for a model of an accountability report, published 14 months after the disaster by Fonkoze). My hope is not just that Fonkoze will get some attention, but that all the anonymous people who labored for years before and after the earthquake inside local institutions that are there for the long haul will be recognized somehow.  I was touched by Time magazine’s choice of “The Ebola Fighters” as the Person of the Year, which reminded me of a time in 1988 when my friend and mentor Michael Rigby observed about the famine of that year in Ethiopia that the untold story was of the heroism of the truck drivers bringing food aid to the hungry despite incredible risks (there were several civil wars there at the time). Too often in international humanitarian work, we focus on the CEOs, the Board Chairs, the donors, the celebrities – and not the rank and file staff and long-term volunteers.

I was touched by Time magazine’s choice of “The Ebola Fighters” as the Person of the Year, which reminded me of a time in 1988 when my friend and mentor Michael Rigby observed about the famine of that year in Ethiopia that the untold story was of the heroism of the truck drivers bringing food aid to the hungry despite incredible risks (there were several civil wars there at the time). Too often in international humanitarian work, we focus on the CEOs, the Board Chairs, the donors, the celebrities – and not the rank and file staff and long-term volunteers.

Fonkoze’s Head Office, Post-Earthquake (Credit: Leigh Carter)

In the case of Fonkoze, which I continue to research a book on while also serving in several demanding volunteer roles, I have been impressed by the drive, vision and results these past five years of people like Marlise Voltaire, Alexandre Hector, Gautier Dieudonne and Dominique Boyer. These four senior staff labor mostly outside whatever small spotlight shines on Fonkoze, but they are the heart and soul of the “building brick by brick” process that I wrote about in my last post to this blog. Two of them are not confident English speakers, so do not represent Fonkoze much internationally; two have worked overseas and could command much higher salaries in more comfortable environs. I am grateful that a small number of patient, caring and flexible donors and investors have been there for Fonkoze during the last half-decade. Their capital combined with a very rigorous internally-driven assessment that began in February 2012 to identify and address institutional weaknesses – especially relating to coordination between the Fonkoze family organizations – is transforming this organization to be ready for whatever the future may bring. I am also grateful to my employer, Grameen Foundation, for giving its blessing to my active involvement in Fonkoze even after its day-to-day institutional involvement was significantly reduced (due to a shift in strategy in the Latin America and Caribbean region unrelated to Fonkoze’s performance). My involvement with Fonkoze at the governance level will conclude next November, after a decade of volunteer service that has allowed me to get to know some extraordinary individuals and learn a lot. Once those roles end, it will allow me to get to work on finishing my book on Fonkoze.

Credit: Leigh Carter

In any case, I will be interested to see how much coverage there is of the fifth anniversary of the earthquake, and what kind of coverage it is. I encourage everyone who was involved with the recovery effort (whether as a volunteer, humanitarian worker or as a donor) to make your voice heard. You can use the comments section of this blog as one place to share your recollections, questions and insights. First Photo Credit: Haiti earthquake of 2010, Photograph, from Encyclopædia Britannica Online, accessed January 01, 2015, http://www.britannica.com/EBchecked/media/151773/A-woman-walking-down-a-devastated-street-in-Port-au

Building, Brick by Brick

Since early 2000s, I have spent a long weekend on the Jersey Shore every six months. Part of my ritual during those visits is to jog north starting in South Belmar (now Lake Como), NJ for several days in a row. My path is along the ocean, which makes it pleasant (if sometimes rather windy). The end of my five mile outbound path is the first section of the Asbury Park boardwalk.

Asbur Park, NJ Boardwalk, in the late 1990s

When I began these runs, Asbury Park was far removed its glory days in the 1940s. Most of the storefronts and former event halls were boarded up. Almost pathetically, people had painted images of thriving restaurants and stores on the walls of the closed stores that faced the boardwalk.

But by the mid-2000s, I noticed that little by little, there were improvements and upgrades noticeable with each passing semi-annual visit. At first they were almost imperceptible. I remember thinking – perhaps heresy for a liberal – that these were evidence of some half-baked urban redevelopment scheme that had already bogged down and would ultimately amount to nothing.

From the late 2000s onwards, it was clear that my pessimism was off base. Asbury Park was coming back. Some said it was because the gay community flocked there and built up quality housing and the ecosystem of stores, restaurants and nightclubs that usually follow. In any case, by the time I jogged on the boardwalk yesterday and earlier today, it was obvious that Asbury Park was booming.

The Boardwalk today

I have noticed that the step-by-step incremental gains that turned Asbury Park from an urban wasteland to a trendy hotspot mirror the arc of building great humanitarian institutions and social enterprises. There are few if any short cuts.

Organizations like Grameen Bank and Fonkoze are built over years, even decades – solid product by solid product, good hire by good hire. Certainly when great products and great talent come along it accelerates things, but those quantum leaps often create problems even as they solve others. (Jealousy in its various forms is often one of them.)

When I look at Fonkoze’s many accomplishments, solid foundation, industry-changing innovations, and resilient nature — particularly in light of my insight about Asbury Park’s revival — I think not so much about any single person, reorganization, value, product, partner or financing, but about the relentless commitment of key leaders to build a better organization, brick by brick.

The gutsy and tireless response to the 2010 earthquake was in many ways Fonkoze’s finest hour. But perhaps that focus shifted the organization’s orientation a bit, from building a great institution to surviving, one quarter to the next. When it was able to break out of this survival mentality for short periods in the post-earthquake period, the focus was on taking big risks – perhaps with the idea that if they paid off, they could make up for lost time in that maddeningly slow process of incrementally building a great institution. While some of those risks worked out, they were essentially negated by those that did not.

The leadership transition in 2013 was probably an inevitable, and healthy, part of moving the organization back to the “three yards and a cloud of dust” process of making Fonkoze at least a little bit better, month by month by month. That shift is paying increasingly visible results, while much remains to be done.

One risk that I have noticed in organizations that are in that relentless slog to build a great institution is that the focus on the next great innovation or recruit can create a sense of alienation among people who have been involved since the early days. Without a conscious effort by leadership, these long-serving loyalists can feel taken for granted. As a result, they can become defensive, hostile to change (and change agents), and even complacent.

Managing this dynamic is, I believe, one of the great challenges leaders face.

Lean Research – Is It Time to Reimagine the Study of Financial Inclusion?

Here is a great blog written by Kim Wilson, who invited me to the “Lean Research” gathering at MIT on August 1.

The Start of a Movement for “Lean Research”?

As I indicated in my last blog, I joined a stimulating gathering last Friday on the topic of “lean research” convened by the Fletcher School at Tufts and D-Lab at MIT. The proposed definition of lean research that the group considered and used as a guide was research that is relevant, respectful, rigorous, and right-sized. (See this blog with helpful definitions of the four proposed criteria for lean research.)

Kim Wilson of Tufts led off the day with a speech that included three examples of what one might call “research run amok.” The first was a case where she had worked for a humanitarian organization that collected a huge amount of data through repeated surveys of poor people, but that used almost none of that information. Another story involved Fonkoze: she explained how she proposed to put a bunch of Fonkoze clients who had survived the 2010 earthquake through a 100-question survey, and how Anne Hastings (then the CEO of one of the Fonkoze organizations) refused to allow it, saying something characteristically blunt and principled like, “My job is to protect my clients, and your job is to extract [information] from them.” In retrospect, Kim saw that Anne was right. Her third major insight prompting this gathering was my blog on the researcher/practitioner interface, which I of course found encouraging.

As I am not a researcher per se, occasionally the conversation last Friday strayed a bit over my head. But it was a diverse group including academics, funders, practitioners, advocates and others, and I learned a lot and felt the vibe was constructive and action-oriented (which I liked). I was asked to give closing comments alongside Amy Smith, the founder of the D-Lab (with which Grameen-Jameel Microfinance Ltd. is working on some exciting action-research in Morocco) and Juan Carlos Rodriguez of USAID’s new Global Development Lab.

Below I have reconstructed (and slightly augmented) the core of my remarks, which Kim encouraged me to make as provocative as possible.

In these closing remarks, I am going to touch on some things that Grameen Foundation and that I can do, and also what I think others should do, related to the discussions we have had today. I will also mention some ideas I have been pushing for years, and others that popped into my head for the first time today. You will notice that my ideas will tend to be fairly simple and practical, though I hope not simplistic – but you, rather than I, will need to be the judge of that.

Why Conduct Research?

My bottom-line framing of this entire issue is related to a basic question: why we do this kind of social science research at all? In my mind, we do it for one reason: in combating societal problems such as poverty, we want to do more of what works well, and less of what doesn’t work, or works less well. Period. If research contributes to that, I will call it successful and effective. If not does not, I will call it a failure – no matter how elegant the research design or how smart the investigators. This is my take on the design principle of “relevance” which we have been discussing today.

I concur with someone who said that research has become too “elite” in that we mostly pay attention to studies that come out of “the best” universities and that follow particular research designs that are in vogue at the moment, designs that some call “gold standard.” I think we need to recognize that valid research can be done through a wide variety of methodologies and sometimes by people with limited training in research methods. The main question in my mind is whether we can learn something useful from research that can help us improve practice or policy.

If we are to deem some research to be the gold standard, that designation should be based on the degree to which the research has led to improved practice or policy, regardless of any other aspect of that research.

Making Research More Accessible

I think it is critical that we demystify research and present it in easier to digest forms, so that those outside the academy, particularly busy practitioners and policy-makers, are more likely to understand and apply the lessons of research. One thing Grameen Foundation has done on two occasions is to commission an academic to analyze the totality of existing research on microfinance and financial inclusion, and then summarize it in a paper running about 30 pages, written in plain English. This has allowed non-specialists, practitioners, policy-makers and others to get a sense of what research says generally about this social innovation, rather than relying on a single statistic, perhaps exaggerated or provided without context, by the media or an overzealous advocate or critic.

Grameen Foundation is going to come out with the third in this series 2015. This gathering reaffirms in my mind the importance of publications like this that make research accessible to decision-makers outside the academy. I encourage others to do so for other fields and other social innovations, as I believe they can help ensure that quality research translates into improved practice and policy.

Another publication I have been advocating for is one focused on “lessons for practice” for those who are providing financial services to the poor. It turns out that many recent studies that looked into the question of whether financial services benefit the poor stumbled onto important insights about how those services can work best. (This insight struck me when reading Dean Karlan and Jacob Appel’s book More Than Good Intentions, which I reviewed on the Center for Financial Inclusion’s excellent blog.) So I have been pleading with the research community to boil those insights down into a single publication that could be read by senior executives and board members of financial service providers to the poor and hopefully influence their service delivery approaches. Finally, one researcher, Tim Ogden of NYU, saw the need and agreed in principle to write it. Still, it remains in limbo for lack of funding – but I am even more committed to getting it done after our meeting here today.

In general, something seems missing in the ecosystem that comprises researchers, practitioners and policy-makers. That “something” would be a person or organization or loose network that saw it as their job to ensure that research makes a tangible, positive difference in the real world. I feel compelled to fill the vacuum in a few cases, and I am sure others are doing their parts. But I think there needs to be a systemic solution. I am not sure what it is exactly. I welcome your ideas.

A Simple Poverty Index

One other insight from today is about the power of a tool that we have helped develop, called the Progress out of Poverty Index®, which has been referenced a few times today. It is a survey tool built to be very lightweight in terms of the demands it places on those being surveyed, and those conducting the surveys. It invariably has ten questions and can be conducted in less than ten minutes. Quite advanced statistics and mathematics are “underneath the hood” of this tool thanks to our talented partner Mark Schreiner. In fact, it is that sophistication which allows for its simplicity in terms of how those who collect and contribute data interact with it.

More tools like this, which are carefully built for robustness and simplicity, are clearly needed. At the same time, we need to leverage existing tools like the PPI® rather than reinvent the wheel, over and over, in terms of survey tool development. Certainly, today’s discussions have increased my commitment to not add more questions to the PPI, as advocated by some.

Four Ideas for Making Research More Relevant

Let me close with four ideas, three that occurred to me just today.

There was talk about giving voice to those being surveyed and studied. I am not sure that involving them in research design and so forth is practical, but I was reminded of something from my years working with Grameen Bank in Bangladesh. Professor Yunus invited many, many researchers in to study Grameen, perhaps viewing their work as a way of augmenting its own monitoring and evaluation capabilities, at little additional cost. But he always insisted that the researchers agree to publish, as part of their final paper, any rebuttal or comment that Grameen wanted to contribute. To my recollection, Grameen never exercised that right. But perhaps it kept the researchers honest from exaggerating their claims or not providing balance and context.

Today, I was wondering if it would be a good practice in published research to not only give organizations being researched the right to do that, but even to insist on it. Let the reader know how the researched institution felt about the process of being studied. And why not take this one step further? What if, as a good practice in respectful research, at the conclusion of the process a representative group of “human subjects” would be assembled and explained what the study found, in language they could understand, and then be asked for their comments on the results and the process. And then their comments would be printed verbatim as an appendix to the study itself. How might this change some of the power dynamics involved in research?

Another idea, which I have proposed before, is to hold researchers to the standard that they rightly hold social innovations and programs to: measure whether they have positive impact, negative impact, or no impact at all. One would assume (or at least hope) that a social program or sector or innovation that had been studied by researchers would be more likely to perform better post-research than pre-research, or compared to programs/sectors/innovations that had not been studied. (If not, why conduct the research?)

Well, if this is our hypothesis, there must be some way to measure whether it holds true in specific cases where research has been conducted. That way we could know what is the impact of impact research. My hope is that it would motivate researchers to spend more time ensuring that their research was being digested and applied before setting off to conduct the next study.

My third idea is to have some credible authority commit to publishing an annual list of the top ten examples of research positively influencing practice and/or policy. Perhaps there could be a cash prize for the top example. Maybe a competing ranking system could spring up if people thought the original list was in any way flawed. My hope is that this could spark new dialogue about how to make research more practical and impactful, by drawing attention and realigning incentives.

Finally, I would like to suggest that this group develop a concise and, to the extent necessary, provocative “declaration” coming out of this meeting. It would state how we feel research should be recast to be leaner, which is to say strike a better balance and application of the principles of being relevant, respectful, rigorous, and right-sized.

Thanks for considering my ideas and thanks especially to Kim Wilson, Kendra Leith and Elizabeth Hoffecker Moreno and their colleagues at Tufts and MIT for their leadership in pulling this important gathering together.

(Update: I strongly suggest people take a look at Kim’s just-published blog on lean research and the August 1 gathering.)

Sensible Microfinance Research, Findings and Media Coverage

It has been a difficult couple of years, in terms of having microfinance researchers, practitioners and the media working together constructively. Naturally, there have been some notable exceptions to this unfortunate trend, and some of the damage has been done despite good intentions, if not outright idealism.

One positive voice in this charged environment has (perhaps surprisingly) been the Economist, which has been fairly balanced as well as engaged during this entire period, having recently written about about a landmark — and controversial — study about the impact of microcredit in Bangladesh that others mostly failed to cover.

But rather than rehash all these difficulties, let me draw your attention to a new article in the Economist. The article makes an obvious and important point (one that is covered towards the end of the blog): a new research report (not to mention common sense) suggests that, at least in the context studied, any given form of microcredit will not be relevant or helpful to all poor people.

To me, this does not mean that entire classes of poor and unbanked people can’t benefit from any form of microcredit or microfinance, but rather that people need to be connected with those products that meet their needs. (Though others could view these findings differently.) In any case, this finding is a strong affirmation of Fonkoze’s approach to segment the poor and serve each segment with a suite of products designed to meet their needs – a concept captured graphically with its “staircase out of poverty.” It also reinforces the concept of “human centered design” as it applies to microfinance, a topic about which Grameen Foundation recently issued an important report.

The main thrust of the Economist article is analyzing a new study that looked at what happened when one group of people was offered microloans and another, comparable group was given microgrants. Basically, those who took the loans benefitted. The same was true of people who were given the microgrants, an approach that is at risk of becoming the next international development fad, or as the Economist terms it, a new “panacea” (but I digress). It is important to note that these were truly microloans (average size: $113) and microgrants (average size: $140). They were given in a very poor environment: rural Mali.

The results were pretty impressive. The Economist summarized them thus: “Both the loans and the grants had clear positive effects among the beneficiaries; more land was cultivated, use of fertilisers increased and profits from self-employment rose in comparison to the families that were given neither.” Furthermore, “the positive effects of both loans and grants that the researchers found show that many poor people face liquidity constraints that prevent them from investing in capital.” [Emphasis added.]

In a second part of the study, some of the people who declined microloans were selected randomly and given microgrants, and there was no measured impact – prompting speculation as to why this was the case. (Above I share my unproven theory, which is that the discrepancy in impact is related to the appropriateness financial products.)

Regarding Fonkoze, this is an endorsement of the idea that for some poor people, grants (often referred to as asset transfers) are the most appropriate product, which is a pillar of the CLM program (the bottom step of Fonkoze staircase). Other studies have confirmed how effective such “graduation programs” can be when they are delivered competently.

Regarding research and microfinance, about which I have written before (such as here), let me note that later this week I will be participating in a seminar on “Lean Research” being pulled together by colleagues at Tufts University and MIT. (Kim Wlson of Tufts talks about “lean research” in this interview.) I am not sure what lean research means exactly; I asked the organizers to define it for me as I prepare my presentation, sparking an invigorating exchange. In general it seems to describe research that is done in practical ways that are designed to maximize the role of – and benefits to – the research subjects, and minimize the costs and other potential negative impacts to those being studied. If it turns out to be an interesting gathering, I’ll report on it in this blog.

Also, Grameen Foundation is working towards publishing a third in its series, “Measuring the Impact of Microfinance” – which is meant to demystify and present in a balanced and non-technical way what recent impact research says about microfinance’s performance and potential. Kathleen Odell has volunteered to do the research pro bono once again (in other words, as part of her academic appointment at Dominican University), and we are raising some money to cover the costs of printing and distributing it in the fall of 2015. So, stay tuned.

CRECER recognized as Truelift Leader

I have written about Truelift, a learning and recognition initiative that Anne Hastings of Fonkoze has served with me on the governing body of. Here is excited news about Truelift’s recognition of a leading microfinance institution in Bolivia that shares many characteristics with Fonkoze.

![]() We are excited to announce that Crédito con Educación Rural, or, CRECER, is the first Latin American organization to achieve the Leader milestone for its adherence to the Truelift Pro-Poor Principles. In the areas of, “purposeful outreach to people living in poverty” and “tracking progress of people living in poverty” this organization has reached the highest possible standards of success in accordance with our principles.

We are excited to announce that Crédito con Educación Rural, or, CRECER, is the first Latin American organization to achieve the Leader milestone for its adherence to the Truelift Pro-Poor Principles. In the areas of, “purposeful outreach to people living in poverty” and “tracking progress of people living in poverty” this organization has reached the highest possible standards of success in accordance with our principles.

CRECER is a microfinance organization based in Bolivia whose mission is to, “offer, with excellence and warmth, financial products along with development services in order to improve quality of life, preferentially of women and their families.” Bolivia ranks 108th on the Human Development Index, measured by average educational attainment, income, and life expectancy; this ranking demonstrates a clear need for pro-poor services.

This rapidly expanding organization, created in 1999, is inspiring hope in the lives of the impoverished, ambitiously reaching all 9 departments in…

View original post 1,143 more words

Human-Centered Design and Other Blog Topics

Believe it or not, but I blog on platforms other than this one. In fact, some of them have relevance to Fonkoze’s journey. Let me highlight a couple of recent ones.

A few days ago I posted a blog related to my visit to J/P Haitian Relief Organization, which was started by the actor Sean Penn in the aftermath of the 2010 earthquake. They use TaroWorks, a technology tool developed by Grameen Foundation (my day job). I was able to tack the visit onto my trip to Haiti for the Fonkoze Family Coordinating Committee, which I Co-Chair. That meeting focused on the importance of Fonkoze being a member-based organization (and what that means in practice), and how SFF was working to increase client retention. As a result of that visit, I encouraged J/P HRO and Fonkoze to consider some areas for collaboration.

I have also published a blog on what I have learned about partnerships through working in the Arab World for the last ten years. After a preamble focused on the history of Grameen Foundation’s work there, I boiled it down to 10 lessons. I referred to this blog during my wrap-up comments at FFCC, since working in partnership — which can be very powerful and terribly maddening — is a central part of the Fonkoze journey, too.

Also on the Grameen Foundation “Insights” blog I wrote about the eMerge Americas conference, which was focused on jump-starting the idea of Miami becoming the Silicon Valley of Latin America. Maybe this vision, if realized, will create opportunities for Haitian-America tech entrepreneurs in Miami?

Lastly, I published a blog about a conference Grameen Foundation organized in Mumbai, India around the concept of user-centered design in financial products, also known as human centered design and client-centered design. Basically, the idea is designing financial products that are the most relevant to the needs of the poor, ideally in a customized way. Doing so could have a major impact on client retention. So could scaling up the Foundation’s adult education modules, so they were available to all clients who wanted them. Anyway, I gave the closing speech at the Mumbai conference and here is the text of my remarks, and here is a final report from the conference in an easy-to-read format.

User-centered design is one way of describing what SFF, in partnership with the Fonkoze Foundation, is doing in an effort to come up with a new generation of products for its members. It is not easy work, but it is what the Haiti’s poor need, and deserve. More than ever, I believe Fonokze has the team in place to design and deliver those products. But it will nonetheless take a massive effort to do so, and perhaps some lucky breaks from Mother Nature in the form of no major natural disasters for another year or two.

This coming Friday is the semi-annual retreat of the Fonkoze Futures Committee, which is focused on fund-raising for the family of Fonkoze organization — essentially spearheading a five-year capital campaign. I have agreed to Chair this group for one more year.

Furthest afield from my work with Fonkoze, I published blogs, such as this one, about my time in Key West celebrating my 20th wedding anniversary with a bunch of my dearest friends, including the Carter Brothers Band who entertained us for seven straight nights with amazing music.